Before you can purchase the home of your dreams, you’ll most likely need to borrow some money from a lender.

Many people have no choice but to take out a conventional mortgage.

However, you may be able to secure much better terms if you understand what an FHA loan has to offer.

What Is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration (FHA) to help borrowers who have low-to-moderate incomes. This makes them an extremely popular option for first-time homebuyers.

While the FHA doesn’t actually issue these loans, their guarantee allows lenders to be far more open to whom they lend.

How FHA Loans Work

As the borrower, you’re actually paying for this guarantee through a Mortgage Insurance Premium (MIP).

You can pick from two types of MIPs to back your FHA loan:

- Upfront MIP: You pay 1.75% of the base amount at the time of closing or have it rolled into the rest of your mortgage.

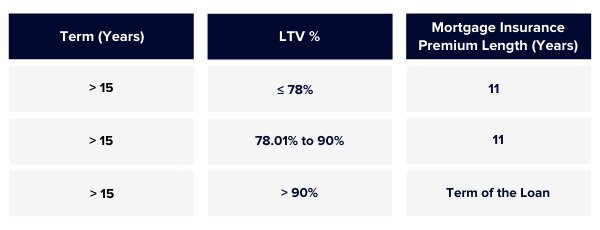

- Annual MIP: You pay every month (despite the word “annual”) between 0.45% and 1.05% of the base amount, depending on the initial loan-to-value ratio (LTV), length of the loan, and total amount.

Here’s a breakdown of how long you’d have to make those annual MIP payments:

You can deduct your premiums, but you’ll have to itemize those deductions. You can’t just take standard deductions to do so.

FHA vs. Conventional Loans

Aside from being backed by the FHA, there are two big differences between these loans and conventional mortgages.

The first is that you can be approved for an FHA loan with a much lower credit score, typically 580 but sometimes as low as 500. For a conventional loan, you usually need at least a 620-640 credit score.

Secondly, the down-payment requirement is lower for an FHA loan, too. You can secure one with 10% down if your credit score is between 500 and 579. However, you only need to put down 3.5% if your credit score is at least 580.

For a conventional mortgage, you’d need at least a 620 credit score to lock in a down payment anywhere near 3%. More than likely, you’d have to put down 10% or more.

The 4 Types of FHA Loans

Aside from the traditional FHA loan we just covered, the Federal Housing Association also offers four other versions you may want to consider.

1. Home Equity Conversion Mortgage

A Home Equity Conversion Mortgage (HECM) is a reverse mortgage program that lets the borrower withdraw some of the equity in their home as cash while maintaining title. It’s designed to help seniors who want to withdraw the money in the form of a fixed monthly amount, as a line of credit, or a combination of the two.

Applicants must:

- Be at least 62 years of age

- Own the house outright or have a minimal mortgage balance

- Live in the house as a primary residence

- Not have any federal-debt delinquencies

They must also go through a consumer information session provided by an HECM counselor.

2. FHA 203k Improvement Loan

As the name suggests, an FHA 203k Improvement Loan can add as much as $35,000 to a standard FHA mortgage, provided the money is used to repair or upgrade the property. These loans are commonly used when an FHA appraiser or home inspector identifies a problem prior to the sale.

However, these loans are actually available to homeowners who have no intention of selling, as well. They can also apply for this loan when refinancing. The lender will simply combine the refinancing mortgage with the funds needed to upgrade or repair the home into a single loan, ensuring a fixed rate with only a down payment of 3.5%.

A 203k Improvement Loan comes with much better terms than high-interest, short-term loans that are often used for improving a house.

3. FHA’s Energy Efficient Mortgage Program

Similar to the 203k Improvement Loan, the FHA’s Energy Efficient Mortgage Program is also designed to help pay for upgrades, but these changes have to result in lower utility bills.

To qualify, the planned improvements have to be cost-effective, meaning the money you save from your lowered utility bills must be the same or greater than the cost of paying for the improvements. A home energy assessment will determine if this is the case before a loan is supplied.

If it’s a new house, the cost-effectiveness of the improvements will be judged based on the most recent International Energy Conservation Code (IECC) standards adopted by HUD for newly-constructed properties.

4. Section 245 (a) Loan

When applying for a mortgage, lenders are going to look at your income. Obviously, this will give them some idea of how much you can realistically pay them back.

A Section 245 (a) Loan is for borrowers who believe their income will soon increase. The program’s Graduated Payment Mortgage begins with lower monthly payments before gradually increasing the amount over time. Its Growing Equity Mortgage is slightly different as monthly principal payments are increased at scheduled intervals, which results in shorter loan terms.

Get Expert Help Securing an FHA Loan

Navigating the complexities of FHA mortgage insurance, FHA loan requirements, and understanding annual mortgage insurance premium rates can be daunting for potential homebuyers. However, the FHA loan program offers more lenient credit scores and lower down payment options compared to conventional loans, making it a popular choice for many. With specific FHA loan limits in place, borrowers can find FHA-approved lenders that cater to their needs, and benefit from reduced mortgage insurance premiums that help lower their monthly mortgage payment.

FHA borrowers should always ensure they work with a reputable FHA-approved lender to secure the best mortgage rates and terms. Furthermore, exploring options such as the FHA energy efficient mortgage can provide additional savings for environmentally-conscious homebuyers.

By comparing FHA and conventional loans and understanding the unique advantages of each, potential homeowners can confidently make informed decisions about their mortgage payment options. Partnering with a reliable FHA lender can make the process of qualifying for an FHA loan smooth and stress-free, allowing borrowers to enjoy the benefits of homeownership with the support of FHA mortgage insurance premiums and the guidance of private lenders.

Even with all of the reasons to love FHA loans, taking out a mortgage is still a big decision. That’s why it’s so important you go about securing one in the best possible way. At SimpleShowing, we will match you with a reputable lender who has been approved by the Federal Housing Authority.

Contact us today and we’ll walk you through the simple process to get started with an FHA loan. Plus, we'll give you $5,000 on average towards closing costs with our Buyer Refund Program.